Know the funds. Now know when to move.

The G, F, C, S, and I funds each behave differently across market cycles. Model Investing’s TSP Allocation Model tells you exactly how to allocate each month, rules-based, no guesswork.

Ready to raise your investing IQ?

Sign up for our Free Newsletter to access the best investment information money can’t buy.

Published On: May 26, 2026

Last Updated: June 8, 2026

The direct answer:

No, the Thrift Savings Plan (TSP) is not technically a 401(k). But it functions almost identically. Both are employer-sponsored, tax-advantaged defined contribution retirement plans with the same annual contribution limits and the same tax options. The critical difference: the TSP is exclusively for U.S. federal employees and military members, while the 401(k) is designed for private-sector workers.

Below is a clear breakdown of how the two plans compare, where they overlap, and what each one means for your retirement strategy.

The Thrift Savings Plan was created by Congress through the Federal Employees’ Retirement System Act of 1986 to give federal workers and uniformed service members the same kind of tax-advantaged retirement savings that private corporations were offering through 401(k) plans.

With more than $1 trillion in assets across over 7.2 million accounts, the TSP is the largest defined contribution plan in the United States. It is administered by the Federal Retirement Thrift Investment Board (FRTIB), an independent government agency. If you’re a federal civilian employee under FERS or a member of the military, the TSP is your primary employer-sponsored retirement account.

For most day-to-day investing decisions, the TSP and a 401(k) operate under the same rules:

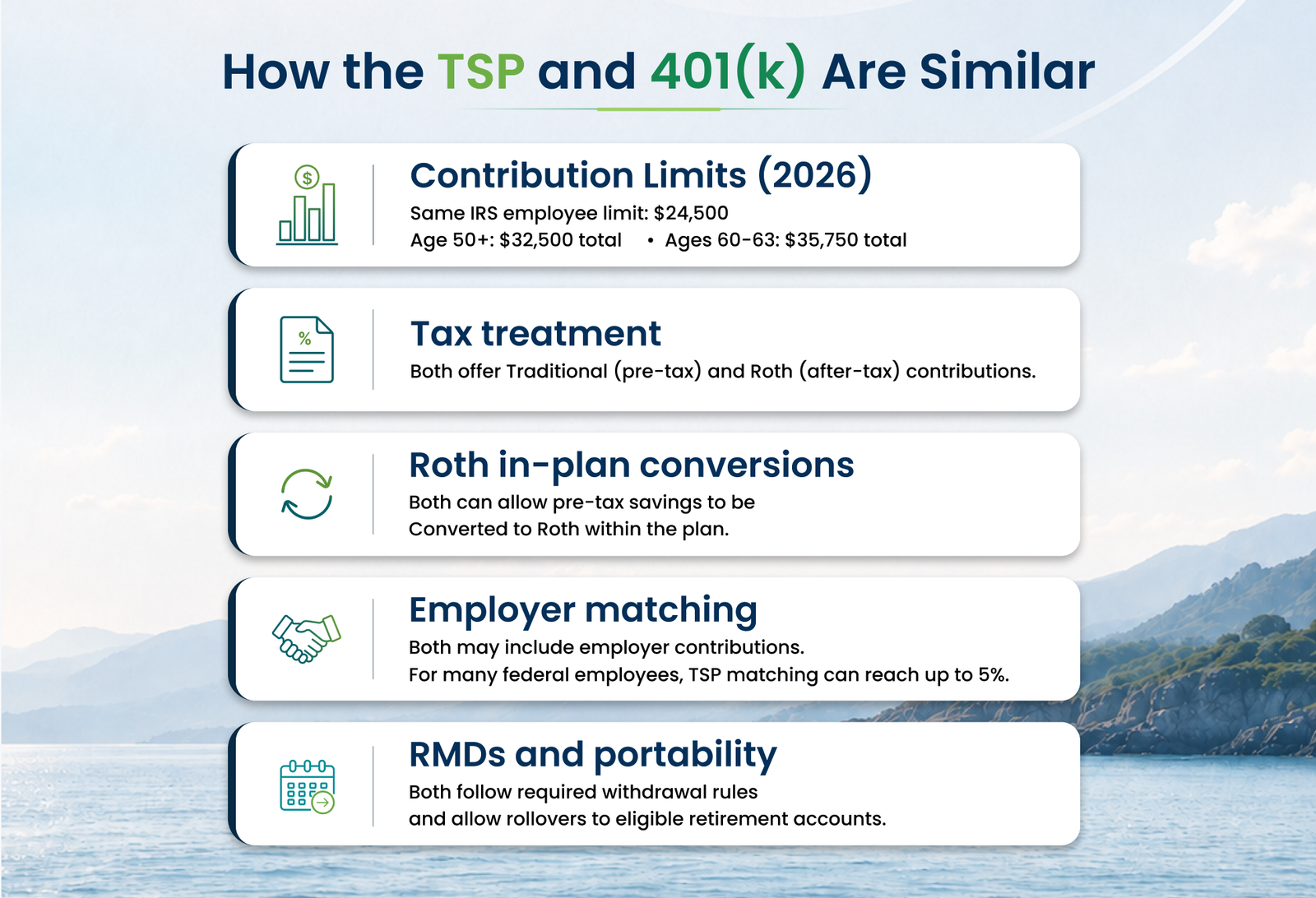

Both plans share the same IRS elective deferral limit of $24,500. Participants age 50 and older can contribute an additional $8,000, for a total of $32,500. Participants ages 60–63 can use the higher SECURE 2.0 catch-up amount of $11,250, for a total of $35,750.

Both offer a traditional (pre-tax) option, where contributions reduce your taxable income today, and you pay taxes on withdrawals in retirement. Both also offer a Roth (after-tax) option, where you contribute post-tax dollars and qualified withdrawals are tax-free.

As of January 28, 2026, the TSP allows participants to convert pre-tax balances to Roth within the account, a feature many 401(k) plans have offered for years. Starting in 2026, catch-up contributions must be made as Roth contributions if the participant’s prior-year eligible wages exceeded $150,000.

Both plans can include employer contributions. Under FERS, the government automatically contributes 1% of your basic pay and matches your own contributions dollar-for-dollar on the first 3%, then 50 cents on the dollar on the next 2%, for a total government contribution of up to 5%.

Both plans require Required Minimum Distributions starting at age 73 (or age 75 if you were born in 1960 or later). Both allow rollovers in and out: You can move a 401(k) into your TSP or roll your TSP into an IRA or a new employer’s 401(k).

This is where the two plans diverge and where federal employees and private-sector workers need to pay close attention.

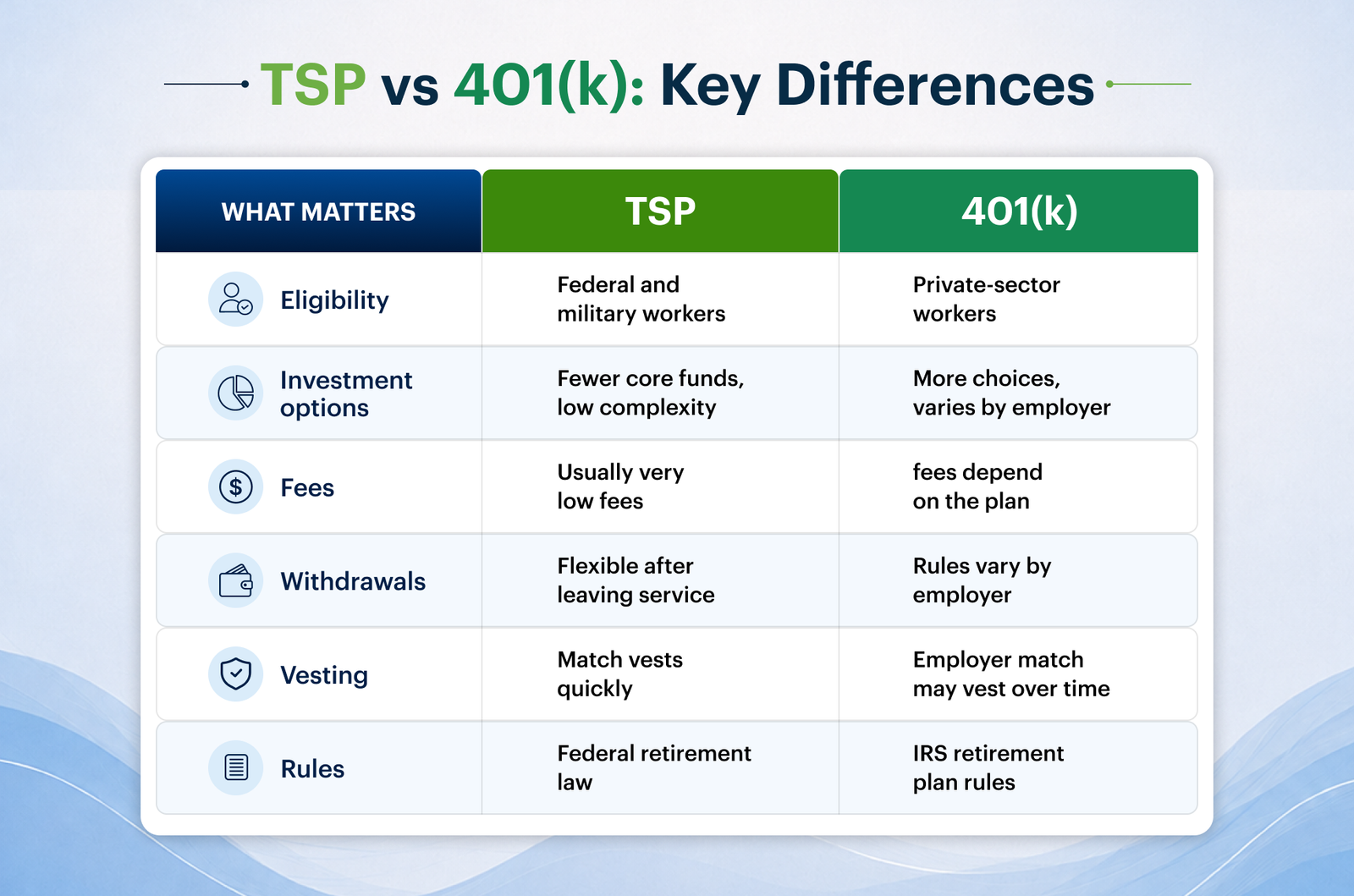

You cannot have a TSP unless you are a federal civilian employee or uniformed service member. You cannot have a 401(k) through the federal government.

The TSP’s standard lineup includes five core funds: G, F, C, S, and I plus Lifecycle (L) Funds and a mutual fund window for participants who want broader access (with added fees). A typical 401(k) plan may offer a much broader investment menu, but the exact lineup varies by employer.

The TSP is one of the lowest-cost employer retirement plans in existence. In 2025, its core funds carried a net administrative expense of about 0.034%. By comparison, 401(k) participants invested in equity mutual funds paid an average expense ratio of 0.26% in 2024 (per the Investment Company Institute). Over a 30-year career, that fee difference alone can mean tens of thousands of dollars more at retirement.

The TSP is actually more flexible in retirement. After separating from service, participants can make multiple withdrawals, and the 30-day waiting period between withdrawal requests was removed on May 15, 2024. Pre-retirement early withdrawal rules are similar between both plans (generally a 10% penalty before age 59½, with exceptions).

Your own contributions are immediately yours in both plans. In a 401(k), employer matching contributions may follow a vesting schedule set by the employer. With the TSP, the agency’s matching contributions of up to 4% are vested immediately, while the separate Agency Automatic 1% contribution requires three years of federal civilian service to fully vest. BRS military participants and FERS employees in certain non-career positions vest in the 1% contribution after two years.

The 401(k) is defined under Section 401(k) of the Internal Revenue Code. The TSP operates under the Federal Employees’ Retirement System Act, which is why some rules differ in nuanced ways.

The G, F, C, S, and I funds each behave differently across market cycles. Model Investing’s TSP Allocation Model tells you exactly how to allocate each month, rules-based, no guesswork.

| Feature | TSP | 401(k) |

| Who it’s for | Federal employees & military | Private-sector employees |

| 2026 contribution limit | $24,500 | $24,500 |

| Catch-up (age 50+) | $32,500 total | $32,500 total |

| Enhanced catch-up (age 60–63) | $35,750 total | $35,750 total |

| Employer match | Up to 5% (FERS): 1% automatic + up to 4% match | Varies (0–6%+) |

| Investment options | 5 core funds + L Funds + mutual fund window | Varies by plan |

| Expense ratios (2025) | ~0.034% for core funds | ~0.26% avg for equity mutual funds |

| Tax options | Traditional & Roth | Traditional & Roth |

| Roth in-plan conversion | Yes (effective Jan 28, 2026) | Yes (plan-dependent) |

| RMD start age | 73 (75 if born 1960+) | 73 (75 if born 1960+) |

| Portability | Rollover to IRA or 401(k) | Rollover to IRA or TSP |

The TSP is your primary tool, and it’s a strong one. The priority is contributing at least 5% of your basic pay to capture the full government contribution, a 1% automatic addition, plus up to a 4% match. This effectively doubles every dollar you put in before any market exposure. Few public-sector benefits are this consistent or predictable.

Beyond the match, your TSP gives you access to extremely low-cost diversified funds. The combination of low fees and meaningful employer contributions makes the TSP one of the most efficient retirement vehicles available to any American worker.

Rollovers are allowed in both directions. You can move an eligible 401(k) balance into your TSP, or roll your TSP into an IRA or new 401(k) when you leave federal service. The TSP’s lower fees often make it an attractive destination for consolidated balances, but the right choice depends on the specific funds, match terms, and flexibility available in each plan.

Some federal employees also have a private-sector 401(k) through a spouse’s plan, a side business, or earlier employment. You can contribute to both a TSP and a 401(k), but your total employee contributions across both plans are still capped by the same IRS annual limit ($24,500 in 2026, plus catch-ups if eligible).

The TSP is not a 401(k), but calling it “the government’s 401(k)” is accurate in every way that matters to your retirement. Same contribution limits, similar tax treatment, and the same basic role as an employer-sponsored retirement plan. What sets it apart is who can use it, how focused the investment menu is, and how little it costs to participate.

For federal employees and military members, that combination of low cost and predictable match makes the TSP one of the strongest retirement accounts available and the foundation of a smart long-term plan.

A strong foundation is just the start. The next step is knowing exactly where to allocate each month. Choose the model built for your plan.

Not exactly. The TSP is not legally a 401(k), but it works in a very similar way. Both are employer-sponsored retirement plans that let you make tax-advantaged contributions, choose investments, and build long-term retirement savings.

The biggest difference is who can use the plan. The TSP is only for federal employees and military members, while a 401(k) is mainly for private-sector workers.

For many federal workers, the TSP can be a better option because it has very low fees and a strong, predictable government match under FERS. Whether it’s better overall depends on the specific 401(k) match, investment options, and plan costs available to the individual investor.

Yes, in some cases, for example, if you work a federal job and also have private-sector earned income. However, your total employee contributions across both plans are subject to the same combined IRS annual limit.

Yes. If you’re eligible for the TSP and have a qualifying 401(k) from a previous employer, you may be able to roll that money into your TSP. Many people consider this because the TSP usually offers lower costs than many private-sector retirement plans.

Yes. The TSP offers both. As of January 28, 2026, it also allows Roth in-plan conversions, letting you move pre-tax balances into your Roth balance without leaving the TSP.

In most cases, yes. The TSP’s core-fund administrative expense was about 0.034% in 2025, well below the average expense ratio for equity mutual funds inside private-sector 401(k) plans (around 0.26%).

You’re always immediately vested in your own contributions and in the matching contributions of up to 4% your agency adds. The separate Agency Automatic 1% contribution vests after three years of federal civilian service for most FERS employees, or two years for BRS military and FERS employees in certain non-career positions.

The TSP offers five core funds: G (government securities), F (fixed income), C (S&P 500), S (extended U.S. stock), and I (international stock), plus Lifecycle (L) Funds. A mutual fund window is available for participants who want broader access.

Neither. The TSP is its own type of retirement plan created under federal law. It shares features with both, but it’s not classified as either one.

The Model Investing Research Team, led by Chief Investment Strategist Matthew Kerkhoff, is a group of finance professionals, data scientists, and software engineers committed to helping individuals make smarter investment decisions. By combining advanced analytics, behavioral science, and market expertise, they simplify complex financial concepts and deliver clear, actionable insights. Their mission is to empower investors of all levels with the knowledge and tools needed to achieve financial stability and long-term success.

Read More

An innovative approach for eaming higher returns with less risk

Download Report (1.2M PDF)You don’t want to look back and know you could’ve done better.

See PricingPosted in