Gender inequality remains a core issue today, and a large portion of the conversation revolves around pay. Women represent nearly half of the workforce, are the sole or co-breadwinner in at least half of American families with children, and receive more college degrees than men. But when it comes to take home pay, they receive, on average, 80% of what a man in a similar position earns.

Ladies – that should frustrate you … a lot. According to the Institute for Women’s Policy Research, based on current projections you’ll have to wait until 2059 to receive equal pay. And if you’re of Hispanic or African American decent, based on current trends, it could take until 2233 or 2124, respectively.

But believe it or not, there’s a different gender gap that’s hurting women even more: The Gender Investing Gap. If you’ve never heard of this, you’re not alone … but it’s real, and in most cases has a bigger impact on overall financial heath than the gender pay gap. The silver lining here is that while you may not be able to close the gender pay gap immediately, you CAN close the gender investing gap. And by making smart investment decisions, you can make up for the disparity in wages and truly outshine your male counterparts!

What is the Gender Investing Gap?

Put simply, women do not invest to the same extent that men do. As a result, when retirement rolls around, women end up with only two-thirds as much money in their portfolios. This is a BIG problem, especially when you consider that women in the U.S. tend to live on average 6.5 years longer than men.

As a result of this unusual dynamic, roughly 80% of women die single, and women are also 80% (yes, 80%!) more likely to be impoverished during retirement. This is a sad statistic and one that needs to change immediately. So ladies, thank you so much for caring for us, our kids, parents and puppies – but please don’t leave yourself out of the equation!

The gender investing gap is the result of three major factors; by addressing each one of these, we can finally level the playing field once and for all:

-

-

- Women earn less than men do – As mentioned above, women receive on average 80% of the pay that men do. So when a man and woman both set aside, say, 6% of their income for retirement, that amounts to 20% less being saved in the woman’s portfolio.

-

- Women don’t save as much as men do – Not only do women earn less, of what they earn, they set aside less for retirement than men do. According to a recent survey by BlackRock, only 53% of women have started saving for retirement. That compares with 65% of men. In addition, of those who have started saving money, women have accumulated less than half the retirement savings as men ($34,900 vs. $76,800).

- Women play it too safe with their investments – Studies show that whereas nearly half of men (45%) are willing to take on high risk with their investments, only 29% of women are. While this is not necessarily a bad thing, it results in women keeping substantially more of their portfolio in cash. And as we all know, cash is an exceptionally poor long-term investment when you consider that it eliminates the magic of compounding, and loses purchasing power to inflation.

-

In addition to these main factors, women often experience reduced employment due to childcare obligations, and this too can have a significant impact on retirement savings. Only about half of women age 25-44 are working full-time, compared with three-quarters of men. While this imbalance tends to level itself out in subsequent years, the fact that women miss out on contributing to retirement accounts during their early years has a dramatic effect – once again thanks to the power of compounding.

Understanding the Impact

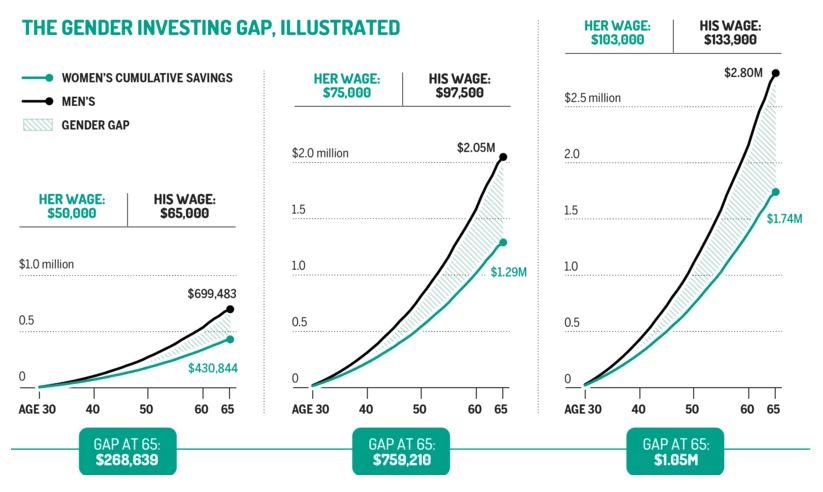

When you take into account all of the factors outlined above, the difference between a man and woman’s retirement can be staggering. The folks over at Time ran through some projections and here’s what they found. Depending on salary levels, propensity to take risk, and a gender-specific salary curve, the gender investment gap over a 35-year career can exceed $1 million. And these figures become even more outrageous when you consider the returns on that extra money that will be achieved during retirement.

What makes this situation even more aggravating is that conventional wisdom suggests that women are responsible for this gap. They’re fed messages such as they’re not as smart or qualified as men, or not as good at investing. But this is total garbage.

Not only are women dominating higher education (earning more college AND graduate degrees than men), studies show that once they do start investing, they outperform men by nearly one percentage point per year. This is because women have a tendency to not over-trade, panic in down markets, or pay too much in fees … In other words, women are kicking ass and taking names – they just need to make a few tweaks to their savings habits to close this gender investing gap once and for all.

What You Can Do About It

The biggest question women have when it comes to investing is: Where do I start? Well, lucky for you, we’ve outlined the most efficient and effective way to save for retirement in our recent post, “How to Save for Retirement.” (Note: this process is the same for both men and women, so men – you can read it too.)

In addition to following the process outlined in that article, women will want to make a few additional adjustments to compensate for their circumstances:

First, set aside a larger portion of your income for retirement than you would otherwise. Since you (unfortunately) earn roughly 80% of what a man in a similar position would earn, you need to set aside about 25% more of your paycheck to make up for this. So if you were going to contribute 4% of your income to your investment accounts, make it 5% instead. That extra 25% will quickly eliminate the effect of the pay gap (at least in terms of your investments) and you’ll hardly notice the difference in your take home pay.

Next, make sure that you’re not “playing it too safe” with your investments. This is one of the biggest problems we see here at Model Investing – investors keep way too much of their portfolios allocated to cash or a stable value fund (such as the G Fund). In effect, these folks are trying to play defense instead of offense, and while that can be a good approach deep in retirement, that money needs the opportunity to grow and compound over the majority of your life.

Of course, we believe that following our Investment Models is by far the most effective way to manage your portfolio, but each investor will have to decide what’s most appropriate for them.

Finally, this last piece of advice applies equally to both sexes, but is especially important for women: Start Early! If you haven’t read this article on compounding, read it now. Albert Einstein is said to have called the power of compounding “the most powerful force in the universe.” You MUST understand this concept if you are to be a successful investor, and once you do, you’ll recognize how foolish it is to put off investing for even another week.

Getting started early is the one surefire way to make up for pitfalls that you’ll experience along the way, such as reduced earnings and savings during child rearing years. You’d be amazed at what a few years of early contributions can do not just for your portfolio, but for your confidence and attitude towards life as well.

A Big Thanks to You

There’s an old saying about women: You can’t live with ’em, but you can’t live without ’em. We find that to be exceptionally true (the latter part at least), and ladies – we would like to take a moment to thank you for everything that you do.

These days, gender inequality is in the spotlight like never before. The #MeToo movement has taken the world by storm and is acting as a catalyst for equality in various ways. Powerful men are losing their power and respect, while powerful women are taking control and getting traction like never before. It’s a remarkable and empowering shift to witness, and this is only the beginning.

This movement also highlights how important it is for women to be financially stable. As Sallie Krawcheck of Time puts it, it’s about being, “Get-your-hand-off-my-leg stable. Take-this-job-and-shove-it stable. Live-my-best-life-stable. Have-as-much-money-as-the-guys-do stable.”

Ladies, you do an incredible job taking care of us, but please don’t forget to take care of yourselves as well. From a financial standpoint, that starts with closing the gender investing gap. So ratchet up those contributions, educate yourself on how to make your money work for you, and let’s watch the balance of power really shift.

The Model Investing Research Team, led by Chief Investment Strategist Matthew Kerkhoff, is a group of finance professionals, data scientists, and software engineers committed to helping individuals make smarter investment decisions. By combining advanced analytics, behavioral science, and market expertise, they simplify complex financial concepts and deliver clear, actionable insights. Their mission is to empower investors of all levels with the knowledge and tools needed to achieve financial stability and long-term success.

Read More

An innovative approach for eaming higher returns with less risk

Download Report (1.2M PDF)You don’t want to look back and know you could’ve done better.

See Pricing